This article has been reviewed by Sumeet Sinha, MBA (Emory University Goizueta Business School). Should you have any inquiries, please do not hesitate to contact at sumeet@finlightened.com.

It can be immensely rewarding if you use credit card responsibly. On the other hand, it can be extremely haunting if do not use a credit card in the right manner. Knowing how to use credit card responsibly can pretty much be the difference between a successful financial life and a stressful one.

How to Read a Credit Card Statement (Jump To Section)

7 Habits of Responsible Credit Card Users

With access to credit, comes responsibility. When you get your credit card in your hand, make sure you develop good credit habits. You can take inspiration from the top 7 habits of responsible credit card users.

Have you checked out our Beginner’s Guide to Personal Finance?

Take note of these 7 habits to use credit card responsibly.

Credit Card Habit 1. Pay Credit Card Amount Due in Full Every Month

Do Not Use Your Credit Card for Any Purchase that you Cannot Afford with Cash Available.

Suppose you have a credit card with an available credit limit of $5000. In your bank account, you have $1000 and the bank requires you to maintain $250 in your checking account at all times. The maximum you can spend with cash is $1000- $250 = $750. Set the same limit on your credit card expenses, irrespective of your ‘credit limit’.

If you spend more than $750, you might have to face a penalty on your checking account for going below the threshold. If you go above $1000, you might have to pay the penalty on your checking account, and/or carry some balance at super-high interest rates on your credit card. It’s not worth it.

Keep the math simple when it comes to using credit cards. Use reasonable amounts on credit cards and automate the payments to be processed before the due date.

Credit Card Habit 2. Weigh the Benefits of Annual Fee Cards against the Annual Fee

Some cards charge an annual fee, and against that provide a set of perquisites such as access to lounges at airports, extended warranty on products purchased, zero foreign transaction fees, etc.

It’s always a good habit to set a reminder before the card renewal fee hits and evaluate whether the fee is worth the perks you are using.

Credit Card Habit 3. Avoid Redundancy of Benefits

Continuing from the point above, if you have multiple annual fee credit cards, evaluate what ‘additional’ perk does each card provides to you. For example, you might have two credit cards, and both offer access to the same set of lounges at airports. Why pay the annual fee on both cards?

Credit Card Habit 4. Do Not Make Unnecessary Purchases to Earn Points

Do not overspend just to earn points. Points are a small fraction of your purchase, and spending more to earn more points is not wise. Instead, think of points as a 1-5% discount on the product.

In some cases it might make sense, i.e. you spend a few extra dollars to qualify for the big sign-up bonus. Even in that case, we’d recommend you look to make advance payments on products and services you’d generally use. For example, can you make an advance payment on your home and car insurance? Can you buy a full year of your Netflix subscription in advance? This way you can put your money to good use as well as spend enough to qualify for the sign-up bonus.

Credit Card Habit 5. Do Not Cycle Credit

Okay, so this is less common, but some people unknowingly do it and risk getting their cards canceled.

So, what exactly is credit cycling? Suppose you have a credit card with a $1000 credit limit, with a statement cycle from 1-30 of the month. On the first day of the month, you buy something worth $1000. The next day you make the payment (because you have the cash to do so!). The credit card will make the $1000 credit available to you again as soon as your payment gets processed. Then, you decide you use the credit card to buy something again. Let’s say you do it two times within the same statement cycle (1-30 of the month in this example).

Bestseller Personal Finance Books

Technically, you are using $2000 credit in one statement cycle. Since you were approved for a $1000 credit limit, the card issuer assumed you’d use an amount up to the credit limit per month. Cycling credit to spend more money per month than the credit limit raises a red flag in the credit card issuer’s fraud detection system, and they may choose to close your account.

Credit Card Habit 6. Keep Credit Utilization Under 30%

Credit Utilization is simply the percentage amount you spend on your credit card out of your credit limit. For a $1000 credit limit card, if you spend $250 on a card per month, your utilization is 25%.

To build your credibility with the credit card issuers, we recommend you maintain your credit card utilization under 30% of your credit limit. This will signal to the credit lenders that you are responsible and help you build a strong credit profile i.e. high credit score!

Credit Card Habit 7. Keep a Tab on Your Credit Score

There are plenty of services that allow you to monitor your credit reports and view your credit score for free. It’s important to keep a tab on your credit reports to identify all your accounts and spot errors if any.

Unfortunately, there are cases of identity fraud where miscreants steal identity and open accounts in other people’s names using their social security numbers and other details. Checking your credit reports to ensure there’s no unexpected credit activity will help fight against such identity theft.

A good credit score can open the doors to easy and cheap financing for your home or car. It is a compelling enough reason to maintain a high credit score because a small decrease in the interest rate of your mortgage can save thousands of dollars for you!

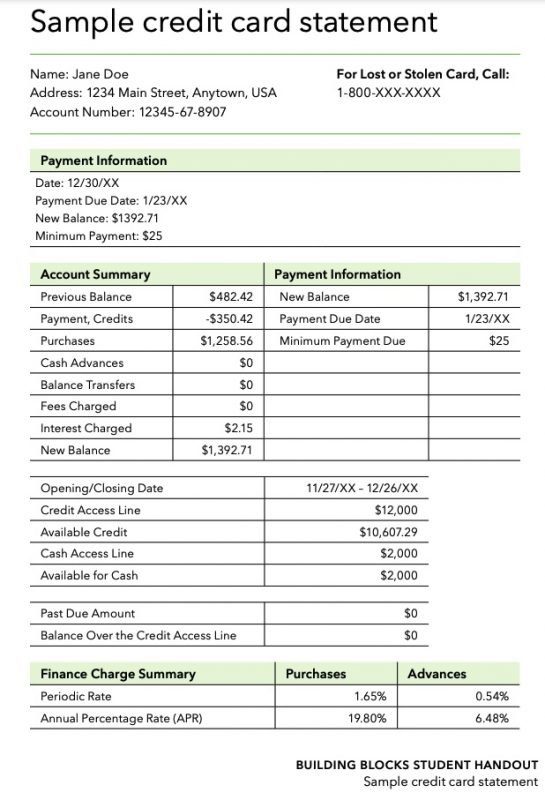

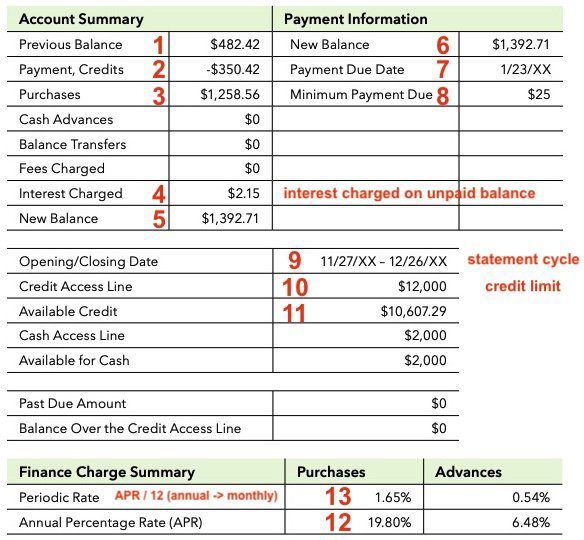

How to Read a Credit Card Statement

This is what a sample credit card statement looks like.

Let’s take a look at some key numbers on the statement.

- Previous Balance: Any unpaid balance from previous statements. $482.42 was not paid by the cardholder and accrued interest during this statement period. (See #9)

- Payment,Credits: Any payments made by cardholder from their bank account to the credit card account. They paid $350.42 during the statement period.

- Purchases: Money Spent on using the credit card, i.e. $1,258.56 used for purchasing products and services.

- Interest Charged: The monthly interest charged on the balance (using interest rate in #13).

- 1.65% * ($482.42 – $350.42 )= $2.17. This number will vary depending on when the $350.42 was paid.

- New Balance: This is simply the unpaid balance + purchases + interest charged

- Thus, New Balance = $482.42 – $350.42 + $1,258 .56 + $2.15 = $1,392.71

- New Balance (essentially the same as 5. above)

- Payment Due Date: The date on or before which you must make the payment to avoid interest and late fees.

- Minimum Payment Due: The minimum payment you must make to avoid penalties or getting reported to credit bureaus for being late on payments. Paying only minimum payment is not advised as you will accrue interest on the unpaid amount. We recommend you pay off the entire statement balance (i.e. $1,392.71 in #5).

- Opening/Closing Date: Statements are generated on a monthly basis, generally. This sample statement if for all activities recorded between the dates 11/27 and 12/26.

- Credit Access Line: Credit Limit given to you on the card by the card issuer.

- Available Credit: Credit Limit – pending balance ($12,000.00 – $1,392.71 = $10,607.29)

- Annual Percentage Rate (APR): Annualized rate on interest on any balance you do not pay by statement due date. (19.80%). As you can see, the APR on credit cards tend to be very high! That is the reason that we advise to never carry balance on a credit card.

- Periodic Rate: Since the statement is generate monthly, the APR is divided by 12 to get the monthly interest rate. (19.80% / 12 = 1.65%)

FAQ on Credit Cards

Should I Carry Balance on my Credit Card?

The Short answer is NO!

Carrying a balance comes with the responsibility of paying back the balance + interest at very high rates (APR). Avoid carrying even a single dollar balance. In our opinion, the best way to use a credit card is to pay it back in full every single month.

If for some reason you are unable to avoid carrying a balance, look for 0% balance cards. Some cards run promotions for 12-15 months. The 0% balance card will give you enough time to come out ahead in the game over time, depending on for much time the 0 balance is in effect.

If at the end of the ‘promotion period’ of 12-15 months you are still unable to pay off the balance, look for a balance transfer card. Balance transfer cards come with fees of 3 to 5% or even more sometimes. So, a balance transfer is also not a cheap option, but it is better than paying 18%+ APR interest on the balance.

Personal loans can be a much more viable option if you qualify for one at a good interest rate. You can take out a personal loan at lower interest rates and pay off the credit card balance, saving hundreds of dollars in interest.

What is Credit Card APR?

APR stands for Annual Percentage Rate. A credit card’s APR is the interest rate you pay for borrowing money i.e. not paying the balance full by the due date. Honestly, credit cards have crazy interest rates, 18% or more in general. Depending on credit score, the interest rates can be more than 30% as well.

APR is an annualized interest rate, so an 18% APR means if you carry a balance of $1,000 for a year, the interest the card issuer would charge you is 18% * $1,000 = $180 (simplified calculation). Generally, the interest is calculated on a daily basis.

So, clearly paying off credit card debt is an instant return on investment of 18%+. That is better than the long-term returns on the stock market which averages at 10% per year!

In order to avoid paying interest, pay all amounts due before the statement due date. Do not carry any balance on a credit card and you won’t have to worry about the APR!

What is a Charge Card?

A regular credit card is approved with a credit limit assigned to it. Charge cards are different in the aspect that it doesn’t come with a pre-determined credit limit. However, that does not mean that there is unlimited spending power available to the user. The purchasing power is determined by the card issuer based on your credit history and spending patterns, but the card issuer does not explicitly mention it to you.

Unlike in the case of credit cards, in charge cards, you CAN NOT carry a balance from one statement to another. You must pay the balance in full at the end of each statement period. If you follow our advice from above (Habit #1), this should not be a problem for you!

Why Should I have a Credit Card?

Credit cards offer various perks to users, such as the following:

- cashless transactions: same as debit card.

- contactless payment options: via contactless cards or Apple Pay, Google Pay etc.

- online shopping: credit cards are accepted at almost all online shops.

- security features such as fraud protection: credit card companies in the US are very good at handling fraud complaints and they protect their consumers’ interests.

- insurance and extended warranty: some credit cards offer theft and damage insurance on phones, some offer rental car insurance, and some offer extended warranty on products purchased with the card.

- lounge access: for frequent travelers free access to a goof lounge can be a great perk.

- reward points: many credit cards offer straight cash back, many have their ecosystem of points such as Ultimate Rewards from Chase or Membership Points from American Express. Users can redeem these for travel, gift cards or statement credits.

- member only events: some credit card issuers host member only events.

- concierge services: premium cards have exclusive concierge service for the cardholders that can get you difficult to obtain tickets or preferred seating etc.

What is a Credit Card Sign-up Bonus (SUB)?

Many credit card issuers run promotions to acquire new customers. They offer a welcome bonus to new customers who sign up for the card and do some qualifying activities such as spending $1,000 – $5,000 in the first three months to earn bonus credit card points or cash back.

Sign-up bonuses can be leveraged if you already have an upcoming expense, and instead of paying in cash or using your old credit card, you sign up for a new card. You can put the expense on it, and earn a higher number of reward points.

How Many Credit Cards Should I Have?

As many as you can responsibly handle. Getting approved for credit cards shows that the card issuer trusts your ability to handle the credit available to you. If you are responsible enough, having more credit available to you should help you keep your credit card utilization at a low percentage level.

If you can follow the 7 credit habits mentioned above and can bear the associated fees, the number of credit cards should not be a problem. You can always evaluate and decide to close a card account if it doesn’t suit your needs anymore.

Conclusion

In order to Use Credit Card Responsibly, one must first learn about credit cards, interest rates (credit card APR), credit card billing cycles, etc. Then, sticking to responsible credit card habits can ensure that one doesn’t fall into a credit card debt trap.

Read more:

- 4 Best Credit Cards For Nannies

- 8 Best Credit Cards for Nurses

- 9 Best Credit Cards for Wedding Expenses

- 10 Best Credit Cards For Consultants

- 8 Best Credit Cards For Golf Lovers

- 6 Best Credit Cards for Traveling Consultants

- How to Use Credit Card Responsibly: 7 Must-Have Credit Habits

- Plastic Money – 3 Huge Payment Networks – Visa, Mastercard, and American Express

- Apple Pay and Google Pay – Which Is Better Among Top 2 Services?

- 8 Cool Benefits of Obtaining A Personal Loan – When to Consider It?

Read more

Popular Topics: Stocks, ETFs, Mutual Funds, Bitcoins, Alternative Investing, Dividends, Stock Options, Credit Cards

Posts by Category: Cash Flow | Credit Cards | Debt Management | General | Invest | Mini Blogs | Insurance & Risk Mgmt | Stock Market Today | Stock Options Trading | Technology

Useful Tools

Student Loan Payoff Calculator | Mortgage Payoff Calculator | CAGR Calculator | Reverse CAGR Calculator | NPV Calculator | IRR Calculator | SIP Calculator | Future Value of Annuity Calculator

Home | Blog

Our Financial Calculator Apps

Page Contents