This article has been reviewed by Sumeet Sinha, MBA (Emory University Goizueta Business School). Should you have any inquiries, please do not hesitate to contact at sumeet@finlightened.com.

Here’s a list of 10 great financial decisions you can make for a better, financially secure life. Take a look and consider implementing most, if not all, of them in your life.

Financial Decision 1. Save for Rainy Day(s)

I like to break the conventional rainy day fund into two parts – a lightning fund and a comprehensive emergency fund.

A lightning fund is for events that need immediate attention like a car breaking down and you need to repair it so you can go on with your life. A lightning fund of $1,000 should be sufficient for most people. Keep this balance in your checking account. This should be easily accessible so that you don’t have to rely on your credit card for such repairs. Of course, you can use your credit card to get some loyalty points, and after that pay off the entire amount due by the due date.

A comprehensive emergency fund is to cover an event that may stay for longer than a few hours or days. Events such as a job loss can stress you out mentally and you can find yourself without a job for a few weeks or even months. The excruciating process of getting hired again is a pain in itself, don’t let money worries further stress you out. Build an emergency fund that can cover ALL your expenses for 4-6 months. Keep this money in a relatively easily accessible account such as a savings account. Do not invest this money in risky assets such as stocks or cryptocurrencies.

Financial Decision 2. Start Retirement Planning Early

You can choose to work till any age you want to, but the earlier you become financially secure (aka have enough funds to live a comfortable life without having to work) the more peace of mind you’ll have.

Irrespective of your age, you should evaluate where you stand in terms of retirement funds and how much would you need to retire comfortably. Will you have to rely on your retirement fund entirely? Do you expect to receive any social security checks? Will you be able to make some income through real estate you own? Asking these questions is critical to retirement planning.

If you are in your early twenties, time is on your side and the money you invest for retirement will compound many times over by the time you reach your retirement age. Understand the retirement programs such as 401(k), IRA, Roth IRA, etc, and start contributing as early as possible.

If you’re in your late fifties, you might have to put away money into retirement accounts to catch up with your target amount. So, evaluating where you stand is always a great idea.

Financial Decision 3. Avoid Credit Card Debt [probably #1 Financial Decision for Many People]

If you have credit card debt, eliminate it on a priority basis. If you don’t have credit card debt, avoid it like plague.

Credit card debt comes at a very high-interest rate, often in excess of 16%. There is absolutely no reason to carry debt with that kind of interest on it. Only buy the stuff you can afford with the money you already have. Do not make purchases on a credit card relying on some money you might get in the future. Even if you pay it back in the next few months, you’ll still pay crazy interest on the purchase. So, it might be wiser to just wait until you have the cash readily available.

Financial Decision 4. Automate Your Bill Payments

Never miss a bill payment on a mortgage, rent, utilities, phone, internet, or credit card. Missed payments or late payments can attract penalties and even interest in addition to penalties. Late payments and missed payments can also dent your credit score. There is so much pain you can avoid by just simply making payments on time.

The good news is almost all the bill payments can be automated. Simply set the option to pay the bills automatically. In case there is no provision for automatic payments, set a recurring reminder on your phone or Google/Microsoft calendar account so you know when it’s time to make the payment.

Financial Decision 5. Understand Your Cash Flow

What gets measured, gets managed. Understanding your cash flow is very important if you want to take control of your finance. It’s important to know how much you are earning, how much you are spending, and WHERE.

Are you spending too much of your income? Are you spending more than your income? How much of the expenses are on things that really matter in your life? How much is just casual expense? It’s a good idea to ask these questions periodically. I won’t decide whether the $4.20 coffee is ‘worth it’ or not, if it matters a lot to you, you get to spend your money on it. Just make sure you know how much money is going where.

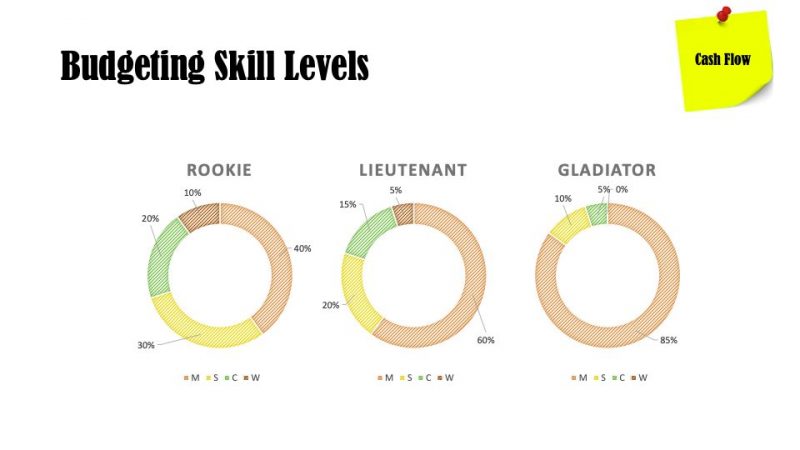

A quick method of categorizing your expenses is the MoSCoW method.

Bestseller Personal Finance Books

Categorize each of your expenses in one of four categories:

- Must Have Items: necessary and non-negotiable expenses (e.g. rent, mortgage, internet, phone etc.)

- Should Have Items: products and services that add significant value to your life

- Could Have Items: things that you deem valuable, but don’t add as much value as in categories above

- Won’t Have Items: things that you can easily live without, and spending money on these is not a wise choice

Create a MoSCoW donut using the data, and see what percentage of your hard-earned money is going in which category of items. The good thing is you can use your judgment to identify which expense falls in which category. As long as you are being honest with yourself, this will be a fair evaluation.

Which one are you? A rookie, a lieutenant, or a gladiator?

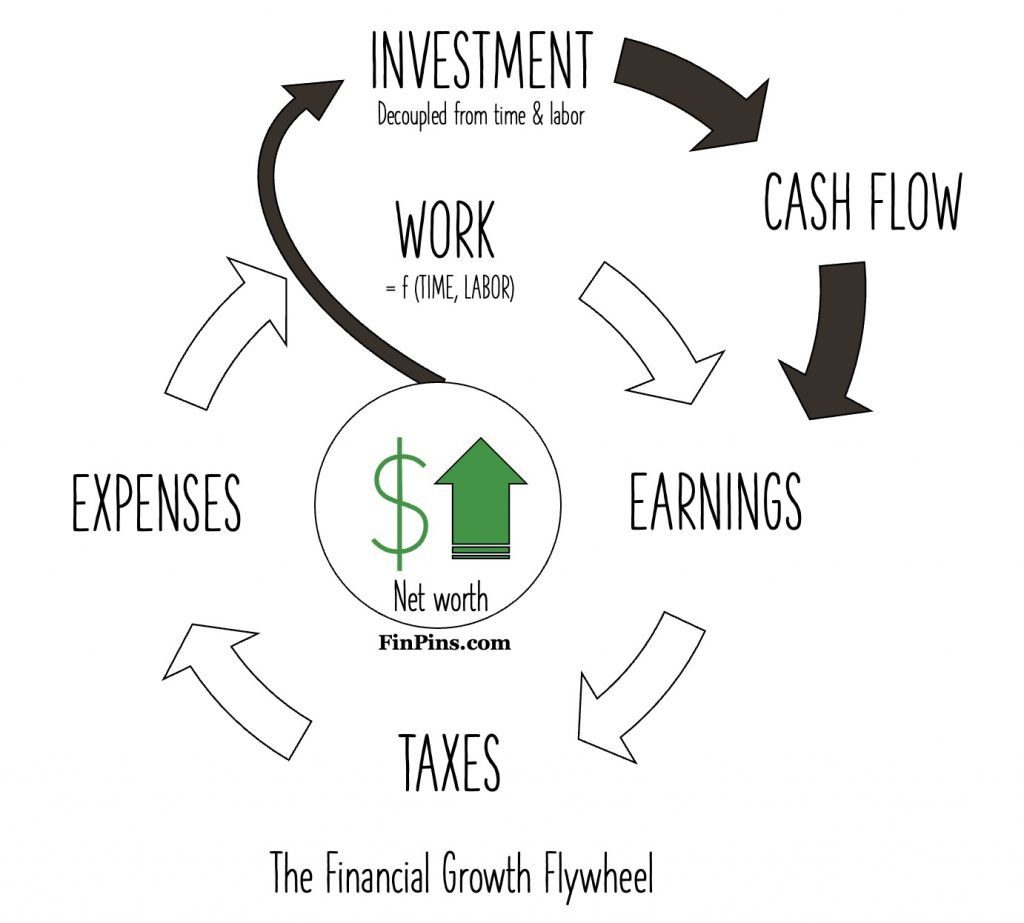

Financial Decision 6. Develop a Growth Mindset

We all love growth – personally and professionally. Why should we not have a growth mindset when it comes to financial matters and growing our net worth? The formula to build wealth is simple. Spend less than you earn, have a positive cash flow, invest that cash flow into something that will generate more cash flow and grow over time.

The Financial Growth Flywheel perfectly demonstrates this.

Financial Decision 7. Pay Yourself First

Here’s the sequence that works best for me.

- Automate all necessary expenses (from M and S categories above).

- Move a certain amount of money to investment account

- Decide on other expenses

- If anything is left over at the end of the month, move that also to the investment account.

Before I make any expenses outside the M and S categories, I pay myself first and commit that money to grow my net worth by spinning the Financial Growth Flywheel.

You can try this too.

Financial Decision 8. Know Investment Options

Don’t procrastinate your plans to start investing. Learn about ETFs, Stocks, and Alternative investments. If you need a quick overview of the investment options, check out this short course on SkillShare. If you don’t have SkillShare membership, use this link to get a free 30-day trial.

If you educate yourself and learn about investing, you can literally save thousands of dollars in advisor and fund management fees and also feel confident about the investing decisions.

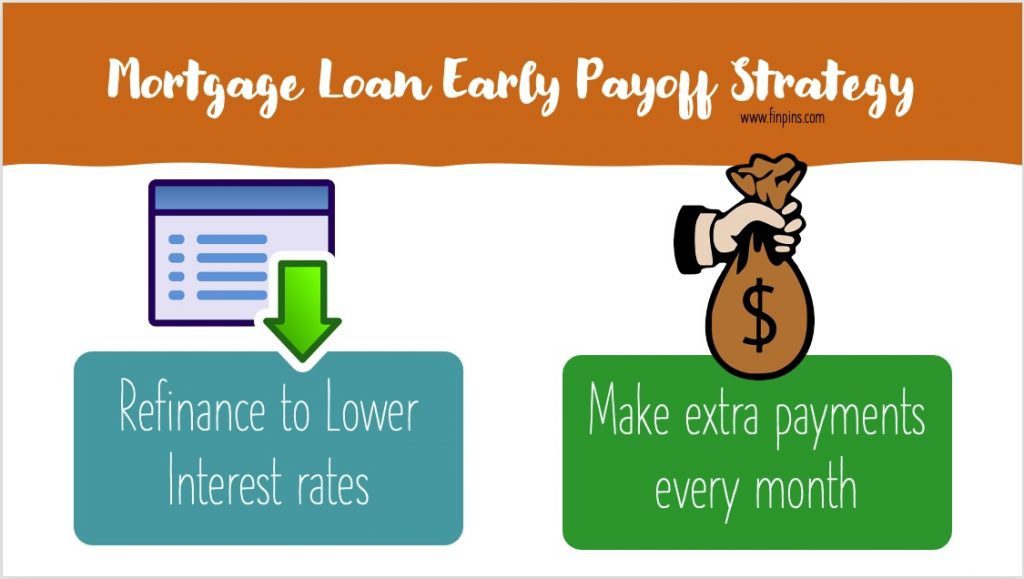

Financial Decision 9. Have a Debt Repayment Strategy

Whether we like it or not, we all end up accumulating some debt at some point in our lives. Student loans, mortgage, personal loans, or even credit card debt – what is the best way to handle debts of all these types?

The smartest way to pay off debts is to make the required payments on all loans, and use some extra dollars to make a dent in the principal of the highest interest loan.

Do you know you can save $34,000 in interest payment just by paying $100 extra every month on a $100k, 25-year loan @7%?

How much can you save by making extra payments? Calculate for yourself here!

Loan Early Payoff Calculator

Financial Decision 10. Learn, Upskill, and Negotiate Your Salary

Getting a college education can open up many doors for you, and get you started on your career path. However, it is very important to keep learning new and relevant things to stay updated with the job market requirements. Be it a formal course at a school, an online course, or learning on the job, always strive to learn new things.

Empowering yourself with the latest knowledge and right skills can put you in demand and increase your salary negotiating power. Do not be afraid of negotiating a better salary for yourself. Prepare a well-crafted value proposition of ‘what you bring to the table’ based on your learnings, and ask for a raise.

If you’re self-employed, the knowledge and skills will set you apart in the market and you can command premium pricing for your services!

Conclusion on 10 Great Financial Decisions To Make

These 10 financial decisions should act as a solid framework for a secure financial life. If you’re just getting started, I’d recommend you check out this Beginner’s Guide To Personal Finance as well.

If you prefer video content, definitely check out my courses on SkillShare. The best thing – you get free 30-day access to not just mine, but thousands of other courses as well. You can cancel anytime.

Read more

Popular Topics: Stocks, ETFs, Mutual Funds, Bitcoins, Alternative Investing, Dividends, Stock Options, Credit Cards

Posts by Category: Cash Flow | Credit Cards | Debt Management | General | Invest | Mini Blogs | Insurance & Risk Mgmt | Stock Market Today | Stock Options Trading | Technology

Useful Tools

Student Loan Payoff Calculator | Mortgage Payoff Calculator | CAGR Calculator | Reverse CAGR Calculator | NPV Calculator | IRR Calculator | SIP Calculator | Future Value of Annuity Calculator

Home | Blog

Our Financial Calculator Apps

Page Contents